By the end of 2024, the DRAM industry is expected to have allocated approximately 250K/m (14%) of total capacity to producing HBM TSV, with an estimated annual supply bit growth of around 260%, says TrendForce svp Avril Wu.

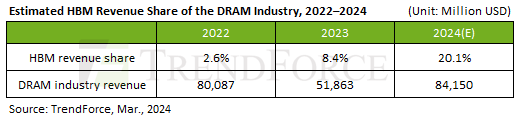

HBM’s revenue share within the DRAM industry—around 8.4% in 2023—is projected to increase to 20.1% by the end of 2024.

The die size of HBM is generally 35–45% larger than DDR5 of the same process and capacity (for example, 24Gb compared to 24Gb).

The yield rate (including TSV packaging) for HBM is approximately 20–30% lower than that of DDR5, and the production cycle (including TSV) is 1.5 to 2 months longer than DDR5.

HBM has a longer production cycle than DDR5 – over two quarters from wafer start to final packaging.

Samsung’s total HBM capacity is expected to reach around 130K (including TSV) by year-end; Hynix’s capacity is around 120K.

Stay up to date with the latest in industry offers by subscribing us. Our newsletter is your key to receiving expert tips.

2026 has entered its second half.Looking back at the first half of the year, the global semiconductor industry continued to evolve under the strong momentum of AI demand. The rapid expansion of AI ser

SEMI's latest forecast projects that global semiconductor manufacturing equipment sales will reach a record US$165.9 billion in 2026, representing a 23.2% year-over-year increase. Driven by sustai

According to supply chain sources, memory contract prices are expected to increase significantly over the coming quarters, with gains likely to exceed previous market expectations.Reports indicate tha