“Geopolitical shifts are fundamentally changing the semiconductor game,” says IDC’s Helen Chiang, “while immediate impacts might be subtle, long-term strategies are focusing more on supply chain self-reliance, security, and control. The industry operation will move from global collaborations to multi-regional competitions,”

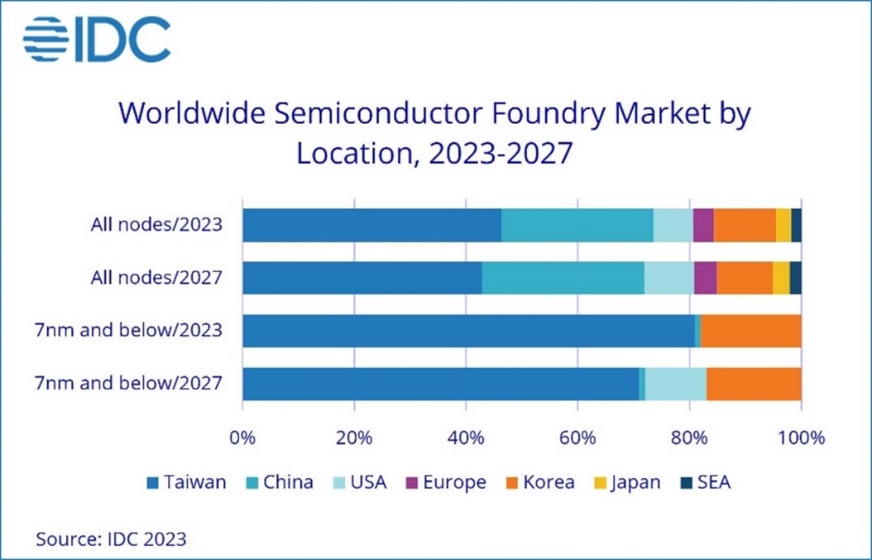

China’s rapid development of mature processes means its proportion of the foundry market will continue to increase, reaching 29% in 2027, an increase of 2% from 2023.

Taiwan’s proportion of the foundry market will fall from 46% in 2023 to 43% in 2027.

The US will make gains in advanced processes, and its share of the foundry market for 7nm and below is expected to reach 11% in 2027.

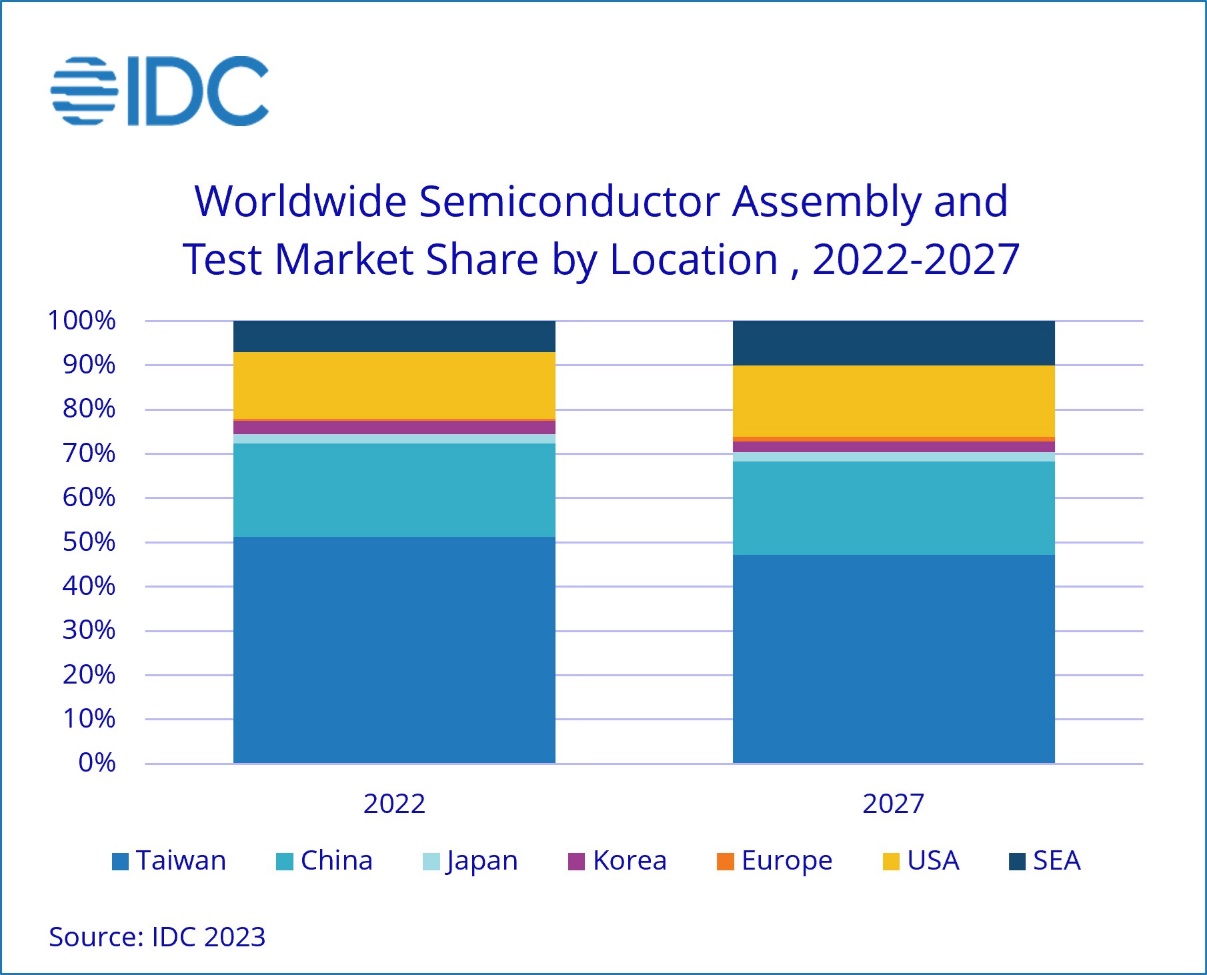

For assembly and test, IDMs have begun to invest more in the Southeast Asia market, and OSAT companies have begun to shift operations from China to Southeast Asia.

Southeast Asia is projected to play an increasingly important role in the semiconductor assembly and test market, especially in Malaysia and Vietnam.

Southeast Asia’s share of the global semiconductor assembly and test will reach 10% in 2027, while Taiwan’s share will decline to 47% in the same year from 51% in 2022.

Stay up to date with the latest in industry offers by subscribing us. Our newsletter is your key to receiving expert tips.

2026 has entered its second half.Looking back at the first half of the year, the global semiconductor industry continued to evolve under the strong momentum of AI demand. The rapid expansion of AI ser

SEMI's latest forecast projects that global semiconductor manufacturing equipment sales will reach a record US$165.9 billion in 2026, representing a 23.2% year-over-year increase. Driven by sustai

According to supply chain sources, memory contract prices are expected to increase significantly over the coming quarters, with gains likely to exceed previous market expectations.Reports indicate tha